By Beijing Hengzhou Bozhi International Information Consulting / QYResearch

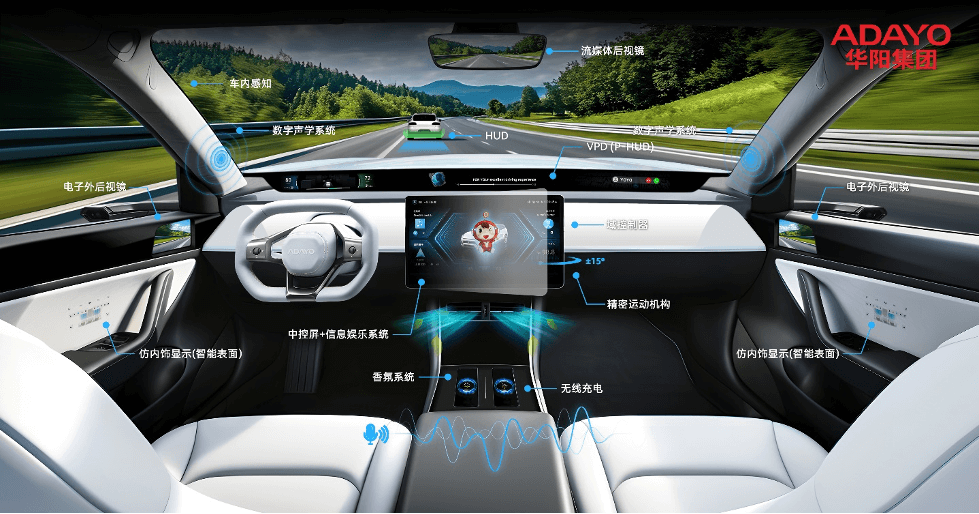

Driven by the continuous rise in intelligent cockpit penetration (with a global intelligent cockpit installation rate reaching 62 per cent in 2024 and 78 per cent in China) and the upgrading of automotive consumption (with the global luxury car sales share increasing to 19 per cent in 2024), laser holographic HUDs (head-up displays), as a core interactive device in intelligent cockpits (accounting for 12 to 15 per cent of cockpit electronic system costs), are undergoing a critical phase of technological differentiation and regional market restructuring. According to the latest data from QYResearch, global sales of laser holographic HUDs are expected to reach USD $1.87bn in 2024 and climb to $3.92bn by 2031, with a compound annual growth rate of 9.8 per cent during 2025-2031. Notably, policy adjustments such as China’s Intelligent and Connected Vehicle Technology Roadmap 2.0 (requiring over 50 per cent HUD installation rate for L3 and higher by 2025) and the EU’s In-Vehicle Display Safety Regulations (mandating minimum HUD brightness of 10,000 cd/m2 by 2027) are reshaping the global laser holographic HUD industry competition ecosystem through technology standard upgrades and cost transmission mechanisms.

• LCOS technology advantages consolidated: Continental’s fourth-generation LCOS-HUD (field of view 15° × 5°, projection distance 2.5 m) combines a silicon-based liquid crystal panel (1920 × 720 resolution) with a laser light source (brightness 15,000 cd/m2), achieving breakthroughs in virtual image clarity and color reproduction. It has been equipped in luxury cars such as the Mercedes-Benz S-Class and BMW 7 Series, with a market share of 47 per cent in 2024, expected to rise to 58 per cent by 2031.

• DLP technology accelerating catchup: The DLP HUD developed by Texas Instruments and Visteon (contrast ratio 2000:1) combines a digital micromirror device (DMD chip size 0.3 inches) with an LED light source (40 per cent lower power consumption). Its penetration in cost-sensitive mid-to-high-end models such as the Toyota Camry is rapidly increasing, with a market share of 23 per cent in 2024, expected to reach 31 per cent by 2031.

The global laser holographic HUD market forms a dual pattern of China leading in growth, Europe leading in technology:

• China market explosive growth: Driven by the wave of intelligent new energy vehicles (NEVs) accounting for 42 per cent of China’s sales in 2024, China’s laser holographic HUD market has surged from $120m in 2020 to $580m in 2024 (31 per cent market share), and is expected to reach $1.43bn (36 per cent market share) by 2031. Typical cases include: Nio ET7 with Zejing Electronics AR-HUD (field of view 20° × 7°, supporting AR navigation), shortening the driver safety warning response time by 0.8 seconds; or the Huawei and BAIC cooperation’s Arcfox Alpha S HI version uses Envisics laser holographic technology (virtual image distance 3.5m), achieving lane-level navigation precise projection.

High-end breakthrough in the European market: German-based Continental (market share 29 per cent) dominates the high-end market through deep integration with BMW and Audi; French-based Valeo’s laser holographic HUD (brightness 20,000 cd/m2) has passed EU certification, supporting the Mercedes-Benz EQS in achieving L3 autonomous driving display requirements. The European market is expected to reach $490m in 2024 (26 per cent share) and $970m by 2031 (25 per cent share).

Lagging technology iteration in the North American market: Constrained by local supply chain limitations (key optical components rely on imports), the U.S. market is expected to reach only $320m in 2024 (17 per cent share). However, the LG laser holographic HUD (field of view 18° × 6°) planned for the Tesla Cybertruck could reduce installation costs through integrated die-cast body design, driving a CAGR of 11.2 per cent in the North American market from 2025 to 2031.

The application field shows a differentiated pattern of luxury car technology benchmark and volume growth in mid-to-high-end cars:

• Luxury car market: In 2024, the installation rate of laser holographic HUDs in luxury cars (price > C¥500,000) reaches 82 per cent. Models such as the Mercedes-Benz S-Class and Porsche Taycan come standard with AR-HUD supporting traffic sign recognition and pedestrian warning, driving a CAGR of 8.7 per cent in this sector from 2025 to 2031.

• Mid-to-high-end car market: Driven by cost reduction (the average price of LCOS-HUD drops to $850/unit in 2024) and policy support (China’s “New Energy Vehicle Industry Development Plan” requires over 60 per cent HUD installation rate for models priced above C¥200,000 by 2025), mid-to-high-end cars priced at C¥200,000 to C¥500,000 have become a new growth pole. The installation rate is expected to reach 31 per cent in 2024 and 68 per cent by 2031. Typical cases include the Denso W-HUD on the Toyota Camry (10° × 3° field of view), reducing driving information reading time by 1.2 seconds. The global laser holographic HUD market forms a ‘3-4’ competitive tier: First tier (technology monopoly): Continental (market share 29 per cent), Nippon Seiki (market share 24 per cent), and Denso (market share 18 per cent) dominate the high-end market through vertical integration (in-house development of optical engines and software algorithms) and patent barriers (over 1,200 cumulative patents), with a combined market share of 71 per cent in 2024.

This report, based on historical data from 2020-2024 and forecast models from 2025-2031, systematically analyzes the global laser holographic HUD market’s technology roadmap (LCOS 47 per cent, DLP 23 per cent, TFT-LCD 19 per cent), regional distribution (China 31 per cent, Europe 26 per cent, North America 17 per cent), and competitive landscape (CR3 reaching 71 per cent). For industry participants, breakthroughs in AR algorithm accuracy (virtual image overlap error <5 per cent) and establishing localized supply chains (domestically sourced core components over 70 per cent) will be key factors for future success.