Gasgoo’s ranking snapshot (January – November 2025) paints a cockpit market that’s both concentrated and rapidly localizing. Local suppliers lead in several key segments (cockpit domain controllers, displays, HUD/AR-HUD, voice), while international players still hold important positions in specific tiers.

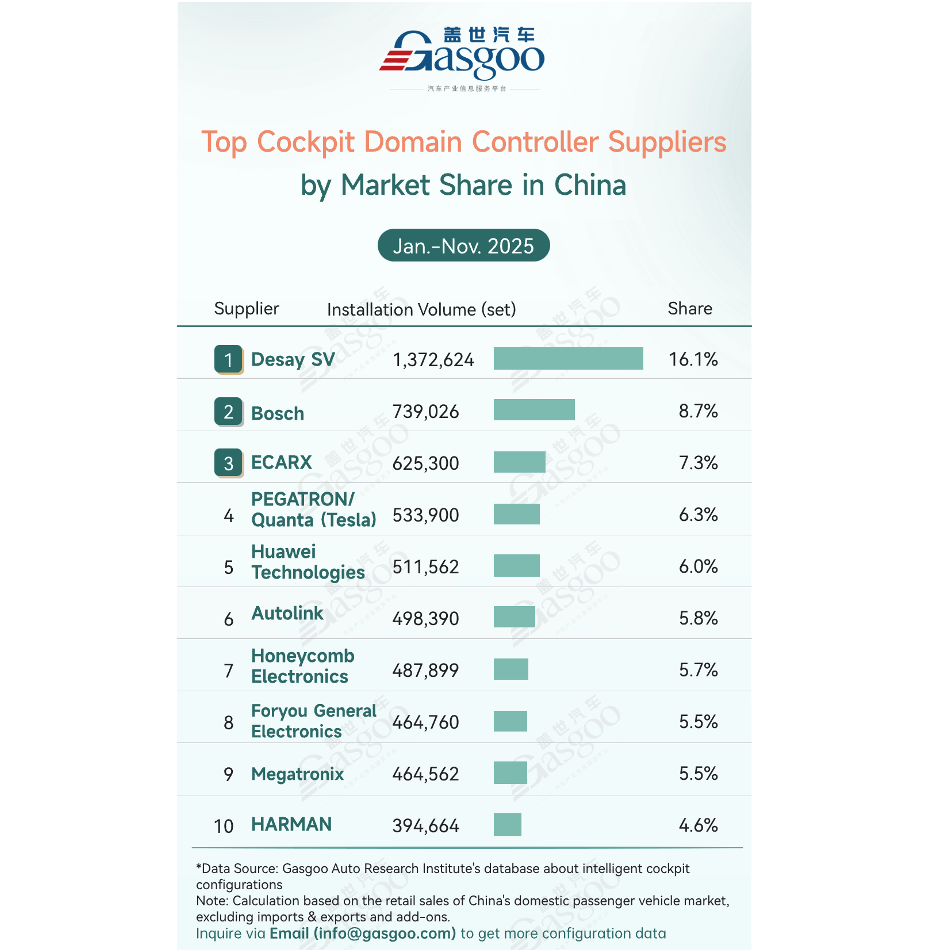

The numbers are the headline. In cockpit domain controllers, Desay SV leads with ~1.37m sets and 16.1-per-cent share, followed by Bosch at ~739k sets and 8.7 per cent. Ecarx sits in the next tier, and tech entrants plus Tesla’s supply chain players widen the competitive landscape.

On cockpit domain controller chips, Qualcomm remains dominant at 73.3 per cent share (~6.37m units installed), but the interesting story is the rising share of Huawei (6.8 per cent), AMD (6.2 per cent), SiEngine (5.6 per cent), and other domestic players. That mix suggests a transition: Qualcomm isn’t being replaced overnight, but the single-vendor-inevitability narrative is weakening.