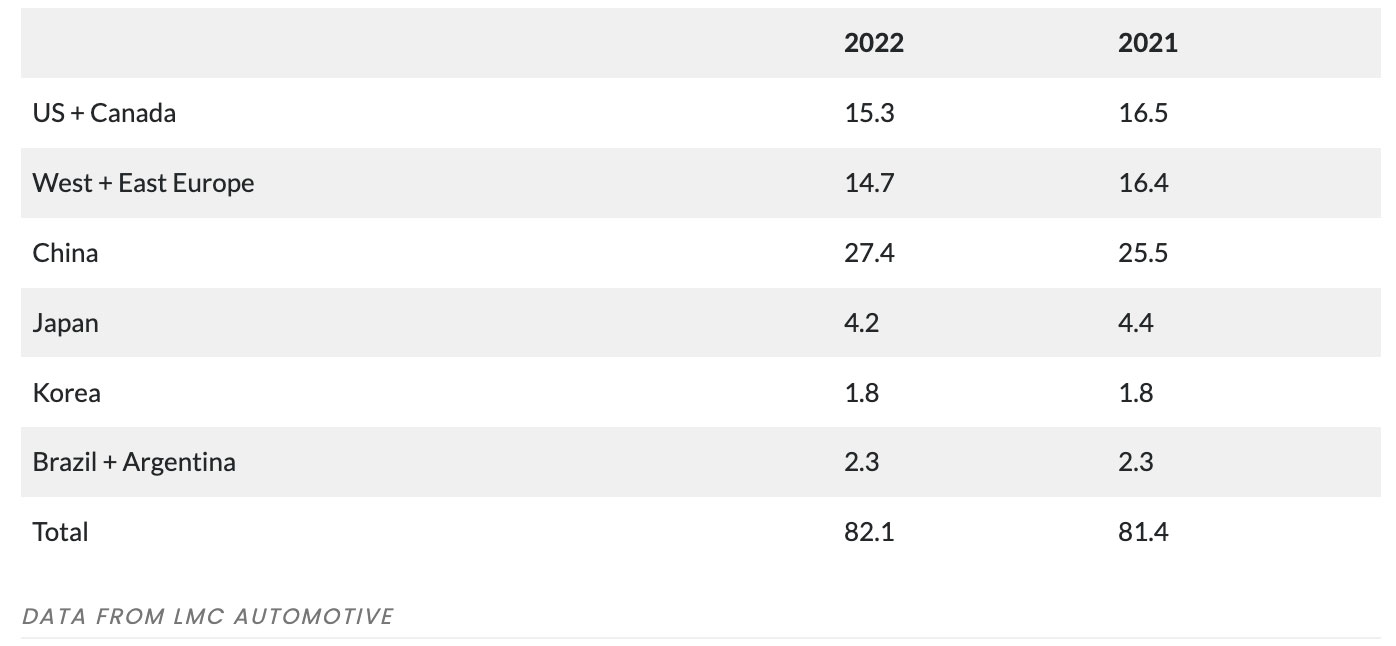

2022 has been a downturn year for the global light vehicle market—projected to wrap up with 82.1 million units sold, about the same as 2021 and 10% lower than 2019’s level of just over 90 million.

U.S. sales grew by 11% to 1.14 million units in November 2022 compared to November 2021. The gain was largely a result of weak sales a year ago, while the selling rate fell from 15.2m units/year in October to 14.2m units/year in November.

Western Europe rose to 13.8 million units/year in November, the second-strongest performance of the year behind August. In raw monthly registration terms, November increased 15%, with 1.1m cars registered.

Eastern Europe grew slightly from the previous month to 3 million units. Despite the increase in sales for November, the market is still down 28% due to the war on Ukraine restricting supplies and sanctions crimping Russia’s sales.

China decelerated sharply in November, amid sporadic lockdowns across the country and an increasingly uncertain economic outlook. Preliminary data indicates that the November selling rate was 24.9 million units/year, down 12 per cent from October. But EVs continued to perform relatively well in China, with sales expanding 58 per cent YoY in November, led by BYD and Tesla. EVs accounted for almost 29% of passenger vehicle sales in the world’s largest auto market.

In Japan, the rate grew to 4.8 million units/year, the highest rate since April 2021. Continuing improvements in component supplies helped boost production and thus sales, especially for miniature vehicles which account for about 40% of total sales.

Korea, too, saw sales hotting up as the year-end expiry nears of the temporary excise tax cut. The November selling rate reached 1.8 million units/year, the highest rate since early 2021, boosted by strong sales of imported vehicles. In contrast, sales growth of domestically built vehicles was modest, despite production having expanded by 25%.